Last Updated on May 18, 2026

Your view of the insurance landscape is changing fast. Today, insurers ramp up digital transformation across workflows and customer touchpoints. About 59% now use generative AI and 75% see ecosystem integration as critical.

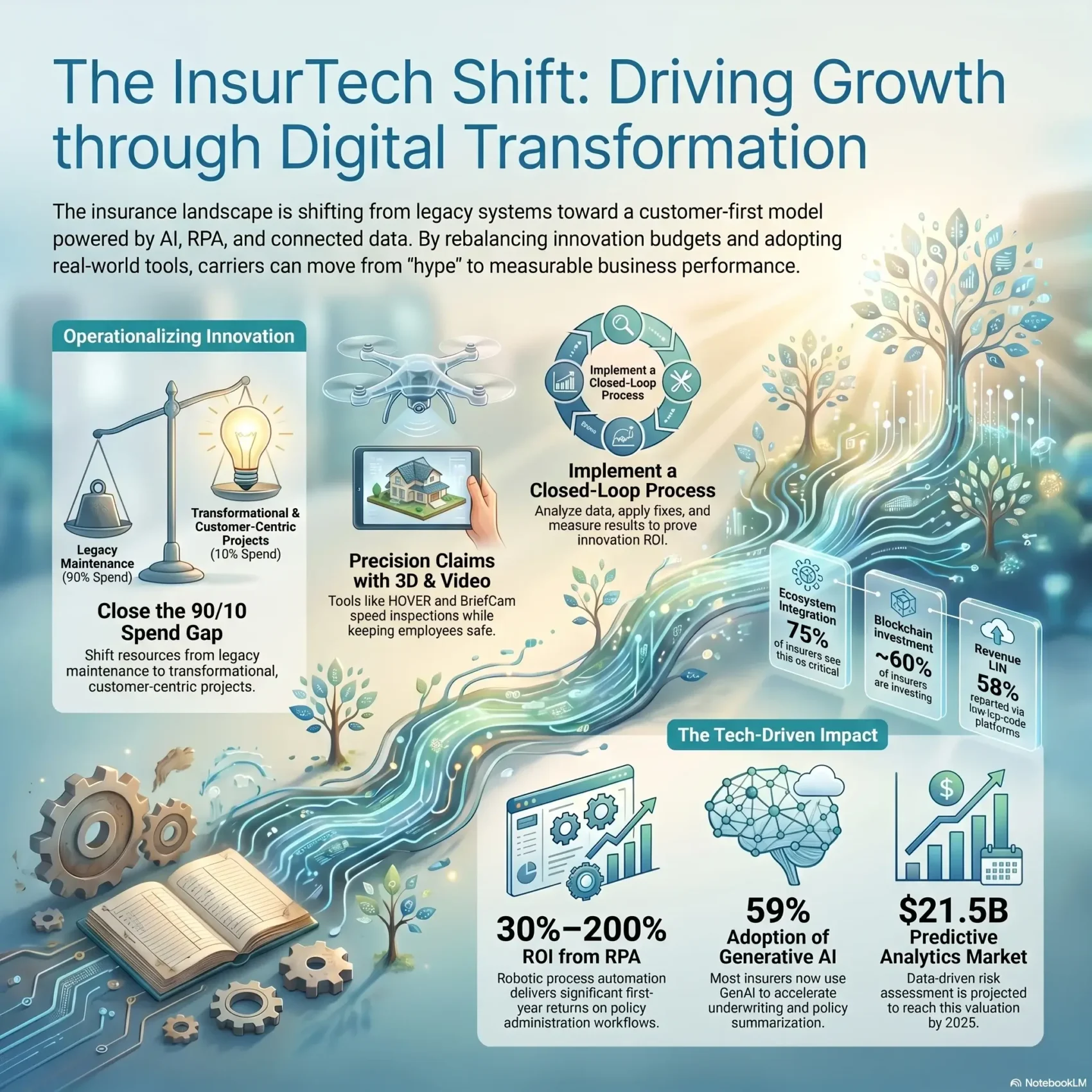

That shift means practical gains: RPA can deliver 30%–200% first‑year ROI, and predictive analytics is set to hit $21.5B by 2025. Companies invest in blockchain (roughly 60% of insurers) and low/no‑code platforms, with many reporting revenue lifts near 58%.

You’ll get a clear view of where the market is moving first — AI, automation, and connected data — and why those moves matter for your customer experience and operating model. Real examples include HOVER 3‑D for faster claims and BriefCam video analytics for safer workplaces.

In short: this section frames what matters now so you can align innovation with measurable growth, not hype.

Key Takeaways

- Digital integration and AI are core priorities for insurers seeking efficiency and growth.

- Automation and analytics deliver measurable ROI and faster decision cycles.

- Connectivity and telematics reshape underwriting and customer touchpoints.

- Low/no‑code and blockchain are becoming mainstream investment areas.

- Real-world tools (3‑D inspections, video analytics) drive faster, safer claims outcomes.

- Treat modernization as a business capability, not a set of isolated projects.

Why InsurTech matters now: your market, your customers, your growth

The United States market is moving toward a customer‑first model that rewards speed, relevance, and clear value. You face consumers whose expectations are shaped by big tech: fast answers, personalized offers, and seamless service.

Deloitte finds many carriers still spend roughly 90% of innovation budgets on legacy enhancements and only about 10% on transformational change. That gap matters because independent agents and brokers still control 83% of commercial premiums, and half of small businesses prefer an agent.

The shift to a customer‑centric insurance industry in the United States

You must balance digital channels with agent expertise. Use analytics to augment frontline workflows so agents sell and serve more consultatively, not replace them.

From data exhaust to decision advantage: turning information into value in real time

Connect legacy systems so information flows where decisions happen. When data informs pricing, underwriting, and service in real time, you lift conversion and retention.

- Prove value: set measurable innovation goals that reassure investors and rating agencies.

- Prioritize: focus analytics where they cut risk and drive growth.

- Assess: run a simple report card across expectations, response time, and personalization to close the biggest gaps first.

“Advanced analytics will grow in value over the next three years for nearly all executives.”

For more context on how market signals influence investment, see startup trends.

InsurTech trends reshaping your insurance business today

Modern technology is rewriting how carriers price risk, handle claims, and serve customers. You can compress decision time, cut operating costs, and launch new service models by combining AI, automation, and connected platforms.

Generative AI for underwriting, claims, and service

Use generative AI to summarize policies, triage FNOL, and surface underwriting insights. About 59% of organizations already use it to speed time‑to‑decision and enable continuous risk models.

RPA and process automation

Robotic process automation handles intake, endorsements, and reconciliations. Expect first‑year ROI between 30% and 200% while adjusters focus on complex cases.

Connected platforms and personalized pricing

Link systems across your ecosystem to build a unified customer view. Combine telematics and analytics to align premiums with individual behavior and improve transparency.

- Fraud detection: pattern analysis flags suspicious claims for human review.

- Chatbots: instant answers free staff for empathy‑first interactions.

- Low‑code & cloud: prototype fast and scale successful products without major reworks.

From pilots to performance: how you operationalize innovation

To move from experiments to steady value, you must organize innovation like any other business line with clear owners and metrics.

Start by rebalancing spend: Deloitte finds roughly 90% of budgets still go to legacy enhancements and only about 10% to transformational work. Create a dedicated team that focuses on new business models and revenue streams. That shift helps your insurance products scale beyond pilots.

Move beyond legacy enhancements

Set strategies that move resources into transformational initiatives. Use a portfolio model to sunset stalled projects and double down on winners.

Partner as co‑developers, not vendors

Structure joint delivery plans and KPIs with external partners so platforms and products are built together. This reduces buy‑and‑drop risks and aligns systems upgrades to customer journeys.

Make innovation measurable and investment‑grade

“Rating agencies now score maturity and expect measurable outcomes, not process descriptions.”

Map an assessment to A.M. Best signals, publish a transparent report for investors, and track cycle‑time, loss ratio, and adoption metrics so leadership can act.

Applied innovation in action: risk, claims, and customer experience

Applied innovation turns routine monitoring into targeted safety action you can measure. Use analytics and remote capture so you spot where risks cluster and act before incidents escalate.

Video analytics: converting surveillance into risk insights and safer workplaces

BriefCam condenses 12 hours of video into about 10 minutes, tagging objects by time and attributes. That searchable synopsis speeds analysis by filtering on vehicle types, size, speed, direction, and faces.

From security camera to risk analysis tool: BriefCam examples you can use today

Heat maps reveal foot-traffic patterns so you can prioritize fixes like barriers or snow removal to reduce slips and falls.

“Faster, easier claims for customers and safer environments for employees.”

Smart property damage assessment: HOVER 3‑D models that speed claims and protect employees

HOVER turns as few as eight smartphone photos into accurate 3‑D property models with precise measurements for siding and windows.

That reduces adjuster site visits and shortens claims time while keeping employees out of hazardous environments. Travelers piloted HOVER in 2018 and completed 100,000+ inspections.

Designing a closed‑loop process: from analytics to interventions to measurable outcomes

Make it a cycle: analyze incident data, apply fixes, then measure results so you prove which changes cut losses and protect employees.

- Use video and 3‑D data to prioritize locations with the highest risk and highest expected return.

- Share insights with facilities and clients so interventions stick and lower incident rates.

- Integrate analytics into claims management to reduce time and improve assessment accuracy.

To explore implementation pathways and partner approaches, see our welcome guide for practical next steps.

Conclusion

Practical adoption of AI, RPA, and connected platforms puts measurable growth within reach.

You can turn this momentum into durable advantage by tying innovation to clear customer outcomes and business metrics. Start with one AI use case, one automated process, and one integration that fixes a high‑friction handoff.

Fund pilots with exit criteria, scale winners fast, and retire projects that don’t lift experience or economics. Use analytics and current data to tune pricing, underwriting, and claims so renewals reflect real risk.

Choose partners that deliver solutions and build internal skills. Report milestones to investors and clients so your company shows measurable progress in the market.

Make next‑quarter moves now — faster decisions, simpler processes, and better service will help your customers feel the difference and grow your business.