Last Updated on April 11, 2026

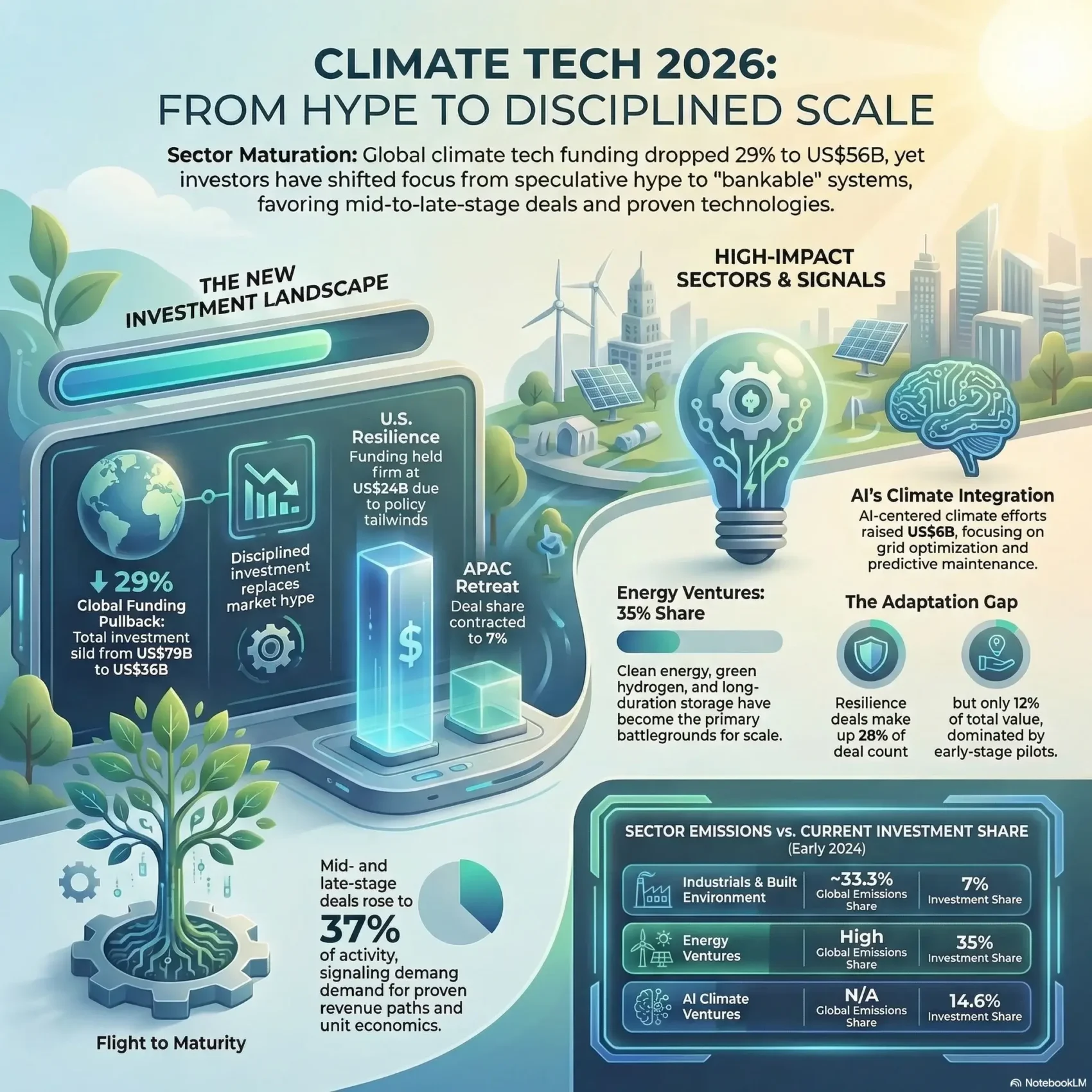

You need a clear, data-driven snapshot of where the market stands and why the tone shifted over the past year. Funding fell notably — total investment slid from about US$79B to US$56B, and share of VC/PE dipped from 9.9% to 8.3% — yet pockets of strength remain.

In the U.S., resilience held steady near US$24B across comparable periods, helped by policy tailwinds. Energy ventures grew their share to roughly 35% in early 2024. Meanwhile, AI-centered efforts raised about US$6B in the first three quarters, and adaptation deals made up ~28% by count.

You’ll learn why disciplined investment is replacing hype, how APAC’s share contracted, and where companies and investors can still win. This piece connects numbers to real decisions so you can judge impact, plan next steps, and spot opportunities in carbon capture, grid upgrades, and startups focused on emissions reduction.

Key Takeaways

- You’ll see clear investment shifts and what they mean for your plans.

- U.S. funding stayed stable; APAC pulled back, changing cross-border strategy.

- Energy and AI plays expanded, while adaptation grew in deal count.

- Discipline in funding favors proven solutions over hype.

- Carbon capture and new platforms matter across industries and businesses.

Executive snapshot: where climate tech stands now

Last year’s numbers paint a clear picture: U.S. activity held firm even as global funding eased. Overall investment fell 29% to US$56B in the four quarters to Q3 2024, and the sector’s share of VC/PE slipped to 8.3%. That pullback hid pockets of strength you should note.

Key signals from the past year in the United States market

The U.S. stayed near US$24B across comparable periods, helped by IRA-driven incentives and stronger corporate demand. Dealmaking moved up the ladder: mid- and late-stage deals rose to 37% of activity in the first three quarters of 2024 from about 20% in 2019.

What changed since the 2019–2024 funding peak-to-trough

Less-experienced investors pulled back, and experienced investors now set a higher bar for returns and proof. Energy and AI-related plays held up better, while industrials softened. Track deal-stage mix, capital intensity, and IRA-linked investments next.

“Dealmaking shifted to mid- and late-stage, rising to 37% in early 2024.”

- Benchmark your raise to mid-/late-stage expectations.

- Focus metrics: capital intensity, customer validation, and runway.

- Watch IRA-driven project pipelines and sector-specific investment pockets.

For deeper signal analysis on startup behaviour and investor focus, see this startup trends overview to align your pitch and timeline.

The market’s changing mood and investment flow

Deal volume and stage mix rebalanced as investors demanded clearer paths to cash generation.

The shift is simple: total financing dropped to US$56B, but mid- and late-stage deals rose to 37% in the first three quarters of 2024 versus ~20% in 2019.

Less-experienced investors pulled back, shrinking their share of deal flow. That left room for seasoned backers who want proven units, revenue paths, and shorter runway risk.

Deal volume, stage shift, and the retreat of inexperienced investors

You should position your raise for mid-stage expectations: clear milestones, unit economics, and real customers.

Why disciplined, returns-focused propositions are winning

Investors now focus on cash generation, margin improvement, and credible scale. Energy and enabling tech drew more interest, while supply constraints still limit rapid growth.

Regional dynamics: U.S. resilience under the IRA vs. APAC mean reversion

The U.S. stayed near US$24B, helped by IRA-driven demand. APAC fell to 7% YTD from 19% last year, so regional strategy matters more than ever.

- Match milestones to funding stage to reduce financing risk.

- Anticipate longer timelines and permitting as core challenges.

- Look for compounding opportunities across wind, grid, and food systems.

“Mid- and late-stage are now the primary battlegrounds for repeatable outcomes.”

Energy technology comes to the fore

Energy-focused ventures captured roughly 35% of funding in the first three quarters of 2024, and that shift matters for your roadmap.

Two large raises — each north of US$1B in green hydrogen and alternative fuels — plus more than 30 clean-energy companies raising ≥US$100M, show buyers and investors backing scale over concept. Mid-stage deals nearly matched late-stage activity, signaling commercial readiness.

Green hydrogen, alternative fuels, and stage traction

You should read the big raises as proof points: project finance and offtake contracts now matter as much as IP. Innovations in electrolyzers and balance-of-plant drove lower capex and opex, reducing carbon intensity and gas-replacement costs.

Where utilities and industrial customers are buying today

Utilities and heavy industry buy bankable systems: guaranteed performance, warranties, and signed offtake. Development milestones — pilots, EPC partners, and supply contracts — de-risk deals and accelerate growth.

- Pack systems with performance guarantees for grid and behind-the-meter buyers.

- Prioritize certifications, interconnection readiness, and safety to win procurement rounds.

- Target corporate buyers in steel, cement, and data centers for scale contracts.

“Bankable systems and clear offtake are the decisive factors for mid- to late-stage investment.”

Hard-to-abate sectors: the industrials, food and agriculture, and built environment gap

You’ll find that sectors driving large emissions still lag badly for funding. Industrials and the built environment account for roughly one-third of global greenhouse gases, yet they fell to 7% of climate tech investment in early 2024 from 17% a year earlier.

This mismatch matters because scale solutions must reach heavy industry, manufacturing, and resource management to move the needle. You should focus on where near-term innovation can deliver measurable returns.

Emissions share vs. funding share: why the mismatch persists

Large capital needs, long payback periods, and difficult retrofits mean companies and investors avoid early bets. Permitting and plant line-change risks add layers of friction.

- Capex intensity: high upfront costs slow adoption.

- Operational risk: downtime and certification hurdles raise barriers.

- ROI framing: energy savings, yield gains, and compliance matter more than just “green.”

Steel, cement, and resource management: near-term innovation pathways

Executives call out steel and cement as urgent priorities. Practical pathways include green hydrogen for process heat, CCUS for point sources, and alternative binders that cut embodied carbon.

- Target pilots that convert quickly to offtake contracts.

- Standardize EPC-ready modules to reduce implementation risk.

- Use MRV and performance guarantees to unlock blended capital.

What you can do: position your solution for measurable cost savings and partner with consortiums to share risk. Watch pilot-to-contract conversions and EPC-standardization as market signals.

For cross-cutting skills and planning that help scale industrial solutions, see this guide on future job skills.

AI in climate tech: productivity, precision, and new risks

You’re seeing AI reshape operations — from self-driving fleets to predictive farm management. AI-related climate ventures raised US$6B in the first three quarters of 2024, about 14.6% of total funding. That flow shows where investors put their focus.

From autonomous mobility to smart energy and agriculture analytics

Autonomous vehicles took the lion’s share of funding (roughly 62%). Industrial applications — agriculture, smart homes, and smart energy — made up about 20%.

- Productivity wins: predictive maintenance and yield optimization cut downtime and costs.

- Grid gains: dynamic load shaping and dispatch models improve asset utilization.

- Operational scale: sector-specific models beat general ones when backed by proprietary data.

Data challenges, MRV, and energy intensity of AI infrastructure

AI relies on high-quality data, and gaps limit MRV and forecasting. Better measurements boost credibility for emissions and carbon claims.

AI models can be energy hungry. Emerging fixes include immersion cooling and heat recycling to cut the infrastructure footprint.

How AI is accelerating emissions reduction and resilience

Use cases translate to measurable impact. You can quantify reductions by linking model actions to meter-level savings or yield gains.

“Investors now ask for proof: measurable savings, shorter payback, and risk controls.”

- Package AI + software with clear compliance and security.

- Show MRV-ready outcomes and per-unit emissions cuts.

- Target procurement paths in utilities, agriculture, and buildings.

Adaptation and resilience move mainstream

Adaptation and resilience have stepped out of niche labs and into everyday budgets. You now see more early-stage deals, practical pilots, and buyer-driven tests that aim to cut real losses and insurance costs.

Deal volume vs. dollar value: adaptation and resilience made up ~28% of deals in the first three quarters of 2024, but only ~12% of total investment value. About two-thirds of those deals were early-stage. That means many small, targeted solutions are winning proof-of-concept rounds rather than huge financing.

Deal share vs. value share: early-stage dominance and what it means

You should plan shorter, milestone-driven rounds. Blend grants, pilot revenue, and corporate partnerships to stretch runway. Investors are betting on many small wins instead of single big exits.

FALU focus: crop resilience, wildfire detection, and insurance innovation

FALU accounts for ~44% of A&R deals. Expect drought-tolerant seeds, stress-detection sensors, and AI wildfire analytics to lead adoption. Insurance products and risk-management services are emerging as clear buyers.

The missing billion-dollar exit and why corporate buyers matter

No billion-dollar A&R exit has emerged yet. Large acquirers can change that by buying pilots and folding solutions into procurement and supply chains. When companies validate performance and pay for avoided loss, valuation follows.

“Focus on measurable resilience ROI — premium savings, avoided losses, and uptime.”

- Structure early rounds with grants + corporate pilots.

- Align MRV and data with underwriters and regulators.

- Target buyers in food, energy, and municipal planning to scale fast.

Carbon capture, utilization, and storage: from pilots to platforms

You can now spot clear pathways where capture moves from bespoke projects to standardized offerings.

Direct air capture, point-source systems, and ocean-based removal are each finding different product-market fits.

Direct air capture is scaling where energy supply and offtake contracts support higher costs. Point-source capture works best at gas-intensive sites and clustered industry hubs. Emerging ocean removal pilots aim for permanence but need robust measurement and policy support.

Utilization routes: concrete, synthetic fuels, and materials

Concrete mineralization (for example, CarbonCure-style injection) already stores carbon while improving strength. Synthetic fuels and advanced materials create revenue paths that help finance capture projects.

- Standardize modules and offtake terms to move from pilot to platform.

- Frame accounting for permanence and MRV to satisfy buyers and auditors.

- Leverage shared infrastructure in industrial clusters to cut costs.

“Investors focus on energy use, cost per ton, and clear scalability signals.”

- Target procurement: industrials, utilities, and municipalities.

- Pursue partnerships with EPCs, storage providers, and offtakers.

- Plan multi-route revenues to improve bankability as you scale.

Grid readiness: storage, load shifting, and renewables integration

Managing intermittent wind and solar at scale calls for long-duration storage and intelligent demand shaping. You need both hardware that holds multi-hour energy and software that steers supply to match demand.

Long-duration storage at system scale

Iron-air and vanadium redox flow batteries now enable multi-hour to multi-day firming. These systems cut curtailment and support high-renewables grids.

Load flexibility and DER orchestration

Distributed energy resources and smart charging coordinate EVs, storage, and demand response.

When you align EV charging with clean supply, you reduce peaks and improve utilization.

Where software and hardware converge

Forecasting, dispatch controls, and real-time telemetry bridge equipment to market signals. Customers expect performance guarantees, warranties, and stable service levels.

- Map permitting and interconnection early to speed deployment.

- Weigh capex vs. opex and pursue revenue stacking for projects.

- Watch utility-owned vs. merchant models—each shifts investor appetite and funding paths.

“System-scale storage plus smart orchestration cuts curtailment and makes wind and solar more bankable.”

Policy tailwinds and uncertainty: the role of the IRA

Tax credits are doing the heavy lifting in today’s project economics, yet election cycles add real underwriting friction.

The IRA’s incentives explain why U.S. investment held near US$24B across sequential four-quarter periods. You should treat tax credits as a core building block when you layer project finance and offtake agreements.

Tax credits, project finance, and corporate demand signals

How credits convert to bankable deals: safe-harbor rules, documentation, and transferability let developers stack tax benefits with corporate PPAs. Those PPAs provide revenue certainty and attract lower-cost capital.

- Align supply chains to capture domestic content bonuses.

- Document timelines carefully to hit safe-harbor windows.

- Use credit marketplaces or transferability to accelerate closes.

Election risk and how investors are underwriting policy exposure

Investors now embed policy scenarios into valuation models. You’ll see term sheets include covenants, step-in rights, and pricing floors tied to credit deliverability.

“Market certainty attracts capital; mitigations matter when policy can change.”

- Price political risk: stress-test IRR and cashflow under alternate outcomes.

- Use insurance, escrows, or sponsor guarantees to bridge shortfalls.

- Communicate exposures clearly to boards and partners so decisions are fast and aligned.

Corporates as climate tech kingmakers

Large corporate players now act as gate-openers, moving promising startups from pilot to production at pace. Corporates took part in about 28% of deals in the first three quarters of 2024, and their backing often skews to mid- and late-stage rounds. That means a company with the right fit can shorten time to market.

Mid- and late-stage capital, pilots, and distribution advantages

Corporate investment — 61% mid/late stage vs. 33% for finance investors — brings more than funding. You get pilots, validation, and access to customers and supply chains.

- Faster validation: pilots convert to paid trials when a company integrates a solution.

- Distribution: corporate channels scale deployments across regions and business units.

- Longer horizons: strategic buyers accept slower payback if the solution fits their operations.

Sector specialization: energy and mobility deals that scale

Companies in energy and mobility attract the most corporate interest. These industries value system integration, warranties, and supply commitments.

- Use JV, licensing, or offtake to align incentives and share risk.

- Pitch on ROI, reliability, and measurable customer outcomes — not just novelty.

- Prepare diligence on safety, compliance, and delivery capacity to win approval.

“Balance strategic partners with financial investors to keep optionality and speed.”

What you can do: map where corporate interest is strongest, tailor your roadmap to energy and mobility buyers, and show clear supply and integration plans to de-risk large deployments.

Funding realities: costs, timelines, and the startup playbook

Funding timelines and real costs now shape the playbook for founders working on deep R&D. You must plan milestones that prove technical progress while keeping burn under control.

High R&D intensity and capital-efficient milestones

Sequence development into short, testable steps. Break large R&D goals into pilots, validation builds, and customer trials.

Use grants and pilot revenue to stretch cash before larger equity rounds. Investors reward clear, measurable de-risking.

Navigating regulation, permitting, and cross-sector partnerships

Map regulatory gates early and run parallel tracks—permitting, safety approvals, and procurement workstreams—to cut schedule slippage.

Form cross-sector partnerships to unlock offtake and co-development. Corporates can shorten timelines and de-risk adoption.

“Sequence milestones so each tranche buys meaningful reduction in technical and commercial risk.”

- Validate performance with meter-level data to meet investor diligence.

- Blend grants, project finance, and equity based on stage and capital needs.

- Set credible buffers in timelines; communicate runway and risks to your board.

climate tech trends

Small but decisive signals now point to who wins the next funding cycle. You should watch five areas where markets, sectors, and capital appetite intersect. These signals help you time raises, pick partners, and sharpen KPIs.

Five signals to watch across markets, sectors, and technologies

Policy durability: U.S. resilience under the IRA keeps project finance alive. Expect safe-harbor timing and domestic-content rules to shape deals.

Stage mix: Mid- and late-stage deals rose to 37%. You should size milestones for proof-of-revenue and shorter runway risk.

Sector rotation: Energy captured ~35% of funding. Hard-to-abate sectors still lag but will attract targeted, bankable pilots.

AI acceleration: Funding nudged from US$5B to US$6B. Investors favor models tied to meter-level savings and proprietary data.

Adaptation mainstreaming: A&R accounts for 28% of deals but only 12% of value. Early-stage pilots dominate; structure grants plus corporate pilots to scale.

What the past tells you about the next funding cycle

Past years show investor appetite moving toward proven outcomes. That means you must prove emissions impact per dollar and stack revenue routes.

“Investors will back companies with clear MRV, offtake paths, and staged dilution.”

- Map policy windows and safe-harbor dates into your funding plan.

- Design milestones that move you from pilot to paid contracts.

- Show meter-level data and blended revenue to make your case.

Future readouts to watch: exits, mega-rounds, regional rebounds, and cross-sector offtake deals. Time your raise when policy clarity, stage readiness, and buyer commitments line up.

Data sources and methodology behind this trend analysis

To interpret the charts, start with how we defined the sample and what counts as an included record. Our dataset grew from ~8,000 to over 12,000 tracked startups in 2024, covering more than 52,000 deals worth over US$600B since 2013.

We included equity and grants from VC/PE (including corporate VC), angels, and government. We excluded debt, asset purchases, and IPOs. Those inclusion rules keep the data consistent and focused on direct innovation.

Definitions matter. We required demonstrable emissions mitigation or adaptation impact for each entry. That first-order impact rule explains why some companies were excluded despite publicity.

Method changes forced us to recalculate historical series for consistency. We also refined sector taxonomy and expanded later-stage and corporate VC coverage to reflect market reality.

- Sources: audited deal records and funding announcements.

- Systems & management: standardized coding and review to improve comparability.

- Guidance: treat outliers and ranges carefully; use medians and bands when you infer risk.

“Transparent methods help you judge signals, not just headlines.”

Knowing these choices clarifies the role and importance of the methodology when you use this analysis to plan and prioritize across the climate tech sector.

Conclusion

strong, The key lesson is that measured innovation and disciplined execution unlock growth even in tight markets. You leave this report with a short set of actions to align strategy, partners, and capital to the next funding window. Use the data to pick where to take action now and what to watch for in the climate tech trends ahead.

Focus on three impact levers: scale energy solutions, crack hard-to-abate industry use cases, and build credible CCUS projects that show clear impact per dollar. Remember U.S. resilience near US$24B, energy at ~35%, AI investment at US$6B, and adaptation at 28% of deals.

For your next steps, test pilots with corporate partners, prove meter-level savings, and tie outcomes to purchase or offtake commitments. That path helps businesses and investors unlock funding and deliver lasting impact into the near future.