Last Updated on June 8, 2026

This introduction gives you a clear roadmap for linking strategy to measurement, disclosure, and real-world value.

You will learn why esg reporting has moved from the margins to the mainstream as investors and communities demand comparable, auditable results.

Major reporting frameworks are set by NGOs, governments, stock exchanges, and industry groups, yet only about a dozen carry broad acceptance.

These tools spell out metrics, narrative elements, format, and cadence. Some are voluntary and some are mandated, so you can match your approach to your risk and market exposure.

Specialized systems automate esg data capture, manage emissions factors from sources like EPA and IPCC, and make sustainability reporting assurance-ready.

When you pair clear targets with strong governance and controls, you improve esg performance and reduce the chance of shareholder action.

Key Takeaways

- You’ll get a roadmap to link corporate sustainability actions with measurement and disclosure.

- Learn why esg reporting has surged and what investors expect from quality data.

- Understand voluntary vs. mandated reporting frameworks and how to choose them.

- Find out how focused materiality avoids confusion from multiple standards.

- See how automated systems make sustainability reporting auditable and repeatable.

What an ESG framework is and why it matters right now

A practical reporting approach shows what to measure, who owns it, and how to tell the story to investors.

An esg framework bundles guidelines, principles, and standards so you know what to track and how to structure disclosures. It acts as a roadmap that turns high-level sustainability goals into concrete KPIs, roles, and year-round controls.

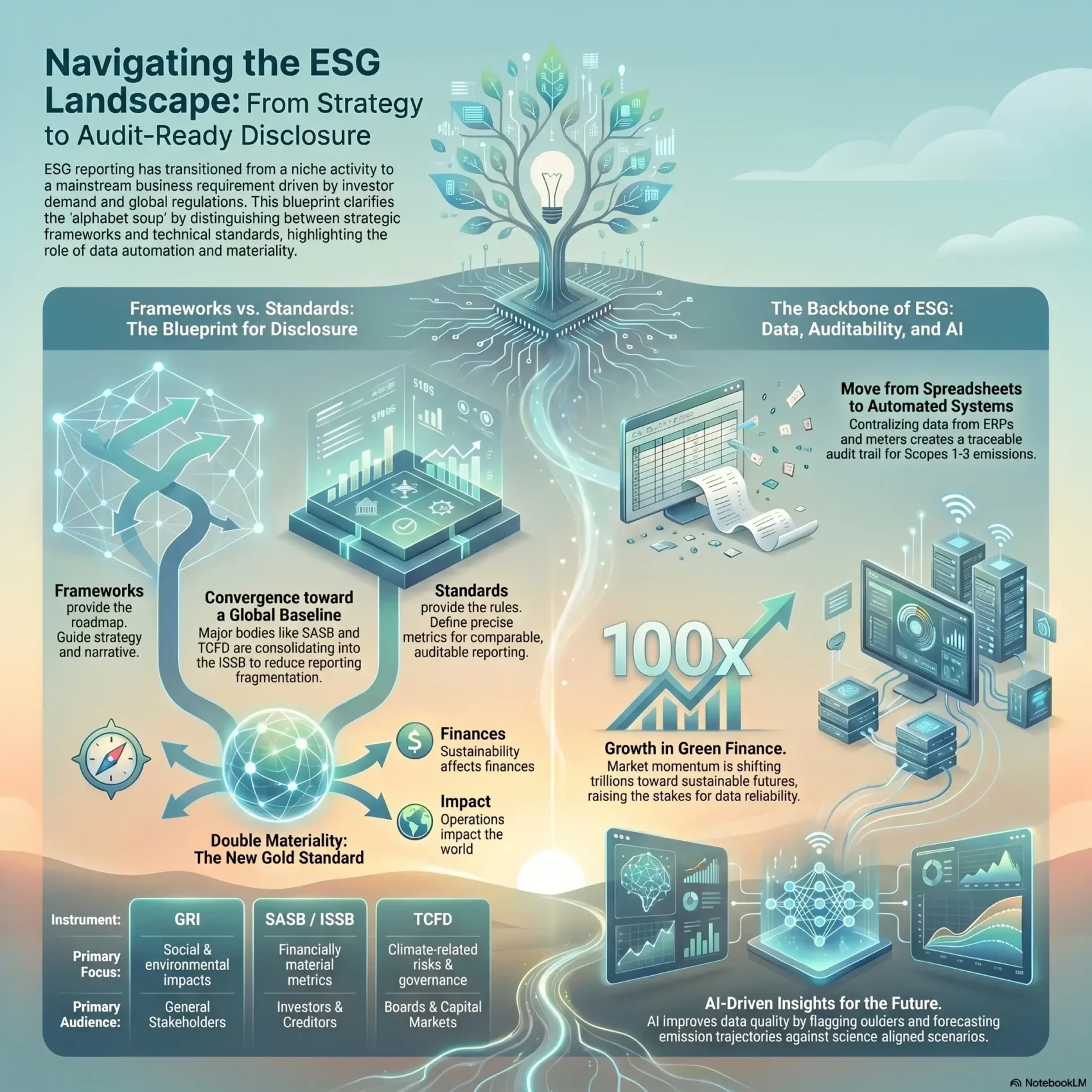

Frameworks vs. the “alphabet soup” of reporting

Not all tools are the same. Some set broad guidance; others require exact metrics. Picking a reporting framework that fits your size, sector, and risk profile avoids wasted effort and data duplication.

How guidance steers strategy, metrics, and disclosures

Use the approach to map esg issues—like climate change, supply chain labor, or data privacy—into measurable targets. That mapping clarifies governance, assigns ownership, and builds investor-grade sustainability reporting.

- Translate policy into KPIs and controls.

- Prioritize material topics and reduce reporting overlap.

- Align disclosures to global reporting norms and task force recommendations.

Benefits: better risk management, clearer benchmarking, and improved access to capital as your disclosures become comparable, auditable, and decision-useful.

ESG reporting frameworks vs. sustainability reporting standards

Standards set the rules for what to report; guidance helps you frame and present the data. A standard specifies quality requirements and public-interest due process so disclosures are comparable and assurance-ready.

Defining the instruments for corporate reporting

Think of a reporting framework as the structure for your narrative and boundaries. It shows how to organize topics and assign ownership.

By contrast, standards define the precise metrics and accounting rules. That clarity supports auditability and makes it easier for investors to compare year to year.

When to use a framework, a standard, or both

Use a reporting framework if your program is new and you need to shape policy and cadence. Add reporting standards as your data controls mature to deliver precise, comparable disclosures.

“SASB, IIRC and related bodies consolidated into the ISSB under IFRS to build a stronger global baseline.”

- Map your policies and KPIs to standards-aligned metrics to reduce future lift.

- Gauge resource needs and assurance readiness early with sustainability accounting checks.

- Layer GRI for impact audiences and industry standards for investor-focused comparability.

Result: a practical reporting architecture that supports current esg reporting needs and adapts as global baselines converge.

From margins to mainstream: today’s ESG reporting landscape

Companies face growing pressure to make sustainability disclosures as trustworthy and timely as financial reports.

Investor and stakeholder demand has surged. You must deliver comparable, accessible, and reliable sustainability reporting so capital providers can judge risk and value. Modern markets treat esg reporting like financial reporting, which raises expectations for controls and auditability.

The rise of standards and mandates

Policy momentum—from the EU reporting directive to U.S. proposals—pushes corporate sustainability toward standardized and sometimes mandatory rules. You should plan for broader scope, stronger governance, and assurance readiness to meet these shifts and climate change disclosures.

Choosing among many options

Pick a reporting initiative that matches your audience: investors, regulators, employees, or customers. Filter the alphabet soup by sector, geography, and materiality to limit costly duplication.

- Make esg reporting repeatable with clear controls and data lineage.

- Prioritize initiatives that map to investor needs and task force recommendations.

- Balance near-term compliance with a scalable strategy to avoid retrofits.

Materiality and double materiality: focus your reporting on what counts

Materiality helps you zero in on the few sustainability topics that actually affect your balance sheet and stakeholders. Use it to decide what belongs in your disclosures and what needs active management.

Financial materiality vs. impact materiality

Financial materiality looks outward: how nonfinancial matters influence enterprise value and investor decisions. Impact materiality looks inward: how your company affects people and the environment.

Apply both lenses so your corporate sustainability reporting captures where value shifts and where social or environmental harm may occur.

Risk matrices and prioritization

Build a simple risk matrix that maps likelihood against consequence. Use it to rank climate-related risks, operational exposures, and policy changes.

“A clear matrix turns broad issues into a prioritized action plan.”

- Score top esg issues by financial impact and stakeholder concern.

- Map risks opportunities for near-term mitigation and longer-term investment.

- Use an action/effort matrix to find quick wins that boost esg performance.

- Document thresholds, owners, and inputs to support assurance and annual review.

Example: an e-commerce company may prioritize packaging waste, supply-chain labor, and ethics. Assign risk owners across functions so priorities are managed day to day, and revisit materiality at least annually to reflect new rules and changing climate-related risks.

Aligning with stakeholder expectations across the value chain

Your disclosures must speak to investors, employees, and regulators in ways each audience values. Start by mapping which reporting tool meets which stakeholder need and then tailor metrics and narrative to that group.

Investors, boards, and creditors: TCFD, SASB, ISSB

Capital providers want investor-grade metrics and climate risk clarity. Use TCFD and SASB-aligned disclosures for climate and financial materiality, and look to the ISSB as a global baseline for comparability.

Employees and customers: united nations and sustainable development goals

Employees and consumers respond to impact themes tied to the united nations and sustainable development goals. Link your culture, DE&I, and product impact stories to those development goals to boost engagement.

Regulators and governments: CSRD, SECR, NGER, SFDR

Regulatory mandates—CSRD in the EU, SECR in the UK, NGER in Australia, and SFDR for financial entities—drive compliance needs. SFDR’s PAI rules, in particular, flow into supply-chain data and reporting obligations.

- Map reporting frameworks to users: investor tools for capital markets; UN SDG themes for staff and customers; local rules for compliance.

- Coordinate data: ensure risk, HR, energy, and procurement teams get tailored inputs—from supplier risk to consumption and DE&I metrics.

- Keep messaging consistent: align annual reports, your sustainability site, and investor decks while meeting each reporting frameworks’ specifics.

“Prioritize themes that matter internally and externally to increase relevance and access to capital.”

Regulatory momentum in the United States and European Union

Regulatory shifts on both sides of the Atlantic are reshaping how companies disclose climate and sustainability information today. You must align your controls, timing, and data so disclosures meet investor and regulatory expectations.

SEC climate-related financial disclosures in the U.S. context

The SEC’s proposals ask U.S. public companies to report climate-related risks reasonably likely to be material. That includes greenhouse gas totals, transition plans, and how climate issues affect your financial reporting cadence and controls.

Make sure finance, legal, and sustainability teams own inputs and that documentation supports audit trails.

EU Corporate Sustainability Reporting Directive and ESRS interoperability

CSRD went into force Jan 5, 2023, widening the scope of corporate sustainability reporting to roughly 50,000 firms. The ESRS, developed by EFRAG, applies double materiality and detailed disclosure modules.

Good practice: map ESRS requirements to your existing reporting to cut duplication and keep investor and impact audiences satisfied.

SFDR and the Principal Adverse Impact statement for finance

For funds, SFDR requires a PAI statement with quantitative indicators. You must calculate financed impacts proportionally—for example, hazardous waste tied to equity share—so your data teams can hand reliable numbers to asset managers.

“Interoperability with the ISSB and recent ESRS–ISSB mapping helps reduce cross-border friction.”

- You’ll translate climate-related financial disclosures into governance, strategy, and metrics.

- You’ll prepare systems for assurance and coordinate owners across finance, IT, and legal.

- You’ll keep optionality to adopt the standards board’s global baseline while meeting ESRS specifics via smart mapping.

Industry and geography: choosing relevant reporting frameworks

Start by matching industry benchmarks to local rules so your disclosures stay relevant and compliant. Your choice should reflect both the sector you operate in and the countries where you have material exposure.

Sector-specific alignment

Use sector tests like GRESB if you manage real assets. GRESB benchmarks real estate and infrastructure sustainability performance and maps to GRI and PRI, so investors can compare apples to apples.

Geographic mandates and local tools

Match reporting frameworks to regional rules—CSRD in the EU, ENERGY STAR in North America, SECR in the UK, and NGER in Australia. This reduces filing risk and surprise compliance work.

- Shortlist esg frameworks that fit your industry to drive sustainability performance.

- Benchmark peers via registry tools and sector filters to set competitive targets.

- Weigh sector-specific rigor against broader impact reporting for a fuller story.

- Watch indices and ratings like jones sustainability that shape investor views.

“Choose the path that gives you comparable metrics for investors and clear proof points for stakeholders.”

Data, auditability, and software: the backbone of ESG performance

Clear data ownership and automated capture are the difference between claims and evidence. Your esg data often lives across meters, ERP, procurement, and spreadsheets. That fragmentation makes greenhouse gas accounting error-prone and hard to verify.

From greenhouse gas accounting (Scopes 1-3) to auditable data

You’ll structure greenhouse gas accounting across Scopes 1–3 with defined system boundaries, named owners, and repeatable calculation methods. Spreadsheets are risky; they lack change controls and audit trails that investors expect.

Automating data capture and emissions factor engines

Specialized software automates meters, ERP extracts, and procurement feeds to produce traceable esg metrics. Emissions factor engines use trusted datasets—eGRID USA, IPCC, IEA, DEFRA, EPA, and national tables—to standardize carbon disclosure and cut errors.

“Build documentation and controls so sustainability reporting can be verified like financial reporting.”

- Centralize disclosures and supporting evidence to speed responses to regulators and investors.

- Harmonize reporting standards and accounting standards once, then map outputs to multiple users.

- Extend controls beyond carbon disclosure to energy, water, waste, and social measures for a full data foundation.

Result: reliable esg reporting, faster close, fewer errors, and stronger investor confidence in your esg metrics.

Inside the leading ESG frameworks and standards

Leading standards each serve a clear purpose: impact communication, investor-focused metrics, climate disclosures, and a global baseline.

Global Reporting Initiative (GRI): impacts and topic standards

The global reporting initiative gives you universal, sector, and topic standards for impact-focused reporting.

Use GRI to tell stakeholders about social and environmental impacts. The revised Universal Standards (2021) and new sector modules — including oil & gas, coal, agriculture, aquaculture, and fishing (2024) — help match disclosures to your material topics.

Sustainability Accounting Standards Board (SASB): industry-specific, financially material

Sustainability accounting standards from SASB cover 77 industry standards across five dimensions.

They help you disclose financially material metrics investors use to compare performance across peers. Apply these standards to strengthen capital-market alignment and investor trust.

Task Force on Climate-related Financial Disclosures (TCFD): governance, strategy, risk, metrics

The task force climate-related guidance structures climate reporting into governance, strategy, risk management, and metrics & targets.

Follow TCFD to make climate resilience and oversight clear to boards and investors. The 2021 updates refine scenario analysis and disclosure practices.

International Sustainability Standards Board (ISSB): the global baseline

The ISSB builds a global baseline by consolidating CDSB and the value-reporting work of SASB and IIRC under IFRS trustees.

Leverage ISSB to reduce fragmentation and map outputs to GRI and local mandates. Interoperability mapping with ESRS (Aug 2023) helps you support multi-market reporting efficiently.

- Practical tip: map overlaps so one dataset supports multiple reporting needs and cuts duplication.

- Align terminology across the standards to keep disclosures consistent and comparable.

- Track exposure drafts and calendars so your reporting stays current.

“Map overlaps among these standards so a single dataset supports multiple disclosures and reduces workload.”

For a deeper look at reporting tools and software that speed adoption, see this short guide on esg reporting trends.

Diving deeper: CDP, GRESB, and Dow Jones Sustainability Indices

Third-party questionnaires turn operational data—energy, water, forests—into market-facing scores and roadmaps.

Carbon Disclosure Project (CDP) collects detailed data through climate, water, and forests questionnaires. Accredited scorers evaluate submissions and sector-specific questions flag high-impact risks and opportunities.

GRESB: real assets benchmarking

GRESB benchmarks real estate and infrastructure with investor-grade metrics aligned to GRI and PRI. Participants get comparative intelligence and clear improvement plans for portfolios.

Dow Jones Sustainability Indices (DJSI)

The dow jones sustainability and jones sustainability indices rank public companies by sustainability performance. Scores influence investor perception and can drive engagement and capital flows.

- Use CDP questionnaires to spot environmental risks and earn scores stakeholders trust.

- Benchmark with GRESB to compare assets and build targeted roadmaps.

- Monitor DJSI results to see how industry peers shape investor views.

- Plan resources for data-heavy submissions and keep public reports consistent with your responses.

“Translate assessment feedback into action plans with clear owners and timelines.”

These reporting frameworks help lift your esg performance and make esg reporting useful to investors and managers alike.

ESG metrics that matter: climate-related financial disclosures and beyond

A concise KPI set helps you show investors how climate risk translates into balance-sheet exposure.

Start with measurable environmental indicators. Capture greenhouse gas emissions across Scope 1–3, plus energy use, water consumption, waste generation, and pollutants. Use clear boundaries, repeatable methods, and published emissions factors so your financial disclosures are auditable.

Also track governance and social indicators: board oversight, ethics, diversity, equity, inclusion, and human-rights steps. TCFD’s focus on governance, strategy, risk management, and metrics/targets helps you link these indicators to enterprise risk and opportunity.

- Core set: GHG, energy, water, waste, and pollutant data aligned to climate-related financial expectations.

- Governance & people: ethics, DE&I, and human-rights KPIs tied to enterprise risk narratives and capital plans.

- Assurance readiness: decide which esg metrics need limited vs. reasonable assurance and build controls and audit trails.

- Transparency: publish Scope 1–3 boundaries, methods, and sustainability accounting choices so numbers repeat year over year.

- Resilience: include scenario analysis and transition plans to explain exposure to climate-related risks.

Result: a compact KPI catalog that maps to investor requests, supports credible esg reporting, and shows how investments drive sustainability performance.

Using multiple reporting frameworks without duplicating effort

Use a single master crosswalk to translate multiple disclosure rules into one repeatable dataset. That approach keeps your team focused and reduces rework when you face overlapping requirements.

Mapping disclosures across GRI, SASB, TCFD, ISSB, and CSRD

Create a map that ties GRI impact items to SASB/ISSB financial metrics and layers TCFD’s governance and scenario outputs. Note the ISSB consolidation of CDSB and the VRF, and use the ESRS–ISSB mapping (Aug 2023) to speed alignment across jurisdictions.

Leveraging existing data to align with reporting standards

Collect once, report many times. Identify common esg data elements, harmonize units and calculations, and assign owners. That single source feeds your corporate sustainability reporting and multiple esg reporting frameworks.

- Build a master map that crosswalks GRI, SASB, TCFD, ISSB, and CSRD to one dataset.

- Define owners, calendars, and controls so submissions don’t overload teams.

- Reuse scenario analysis, governance text, and risk registers with minimal edits.

- Harmonize calculations to cut reconciliation and audit findings.

- Prioritize disclosures that satisfy most stakeholders, then fill gaps.

- Document assumptions so you manage risks opportunities consistently across outputs.

“A clear crosswalk turns multiple reporting obligations into one efficient process.”

What’s next: AI, consolidation, and the future of sustainability reporting

AI is reshaping how companies clean, check, and use sustainability data at scale. You can use models to speed data checks, spot anomalies, and benchmark performance across peers.

Applying AI to data quality and decision-making

AI improves data quality by automating validation, filling gaps, and flagging outliers so your esg reporting is faster and more reliable.

It also links sustainability metrics to financial outcomes, helping you quantify how climate change and other risks affect capital allocation.

Practical guardrails and uses

- Use bias checks, privacy controls, and efficiency metrics to reduce AI risk.

- Forecast emissions trajectories and test target pathways against science-aligned scenarios.

- Design modular data systems so new rules or metrics plug in without reengineering.

Convergence under global standards

The standards board (ISSB) and collaboration with the global reporting initiative aim to reduce fragmentation. Aligning accounting standards and interoperability mapping with ESRS will help rationalize your reporting frameworks and cut duplication.

“Use AI to move from manual reconciliation to insight-driven corporate sustainability decisions.”

Result: streamlined esg reporting that saves time, reduces cost, and strengthens governance as convergence progresses.

Conclusion

, Clear, auditable reporting turns sustainability commitments into measurable business value.

You’ve seen how standards like ISSB and ESRS, plus bodies such as GRI, SASB, and TCFD, are pushing standardized, auditable disclosure. Use technology and strong data controls to make your corporate sustainability work repeatable and verifiable.

Now you can pick an esg framework that fits strategy and sector, structure sustainability reporting around material topics, and report esg with investor-grade rigor. Embed sustainable development in everyday decisions so voluntary esg steps scale into measurable outcomes.

Result: better esg performance, clearer stakeholder narratives, and corporate sustainability that drives risk management and growth—not just compliance.

in SaaS")