Last Updated on June 2, 2026

You’re reading about a policy that rose to public view during the pandemic, when stimulus checks exposed gaps in support and job volatility.

This idea — championed by figures like Andrew Yang and local leaders such as Michael Tubbs — frames cash payments as a steady floor for households. Jack Dorsey and civic pilots in cities like Durham and Stockton showed how private funds and local governments test real effects.

Researchers Fabian Wendt and Doug MacKay call unconditional cash a platform to build life on, not a full substitute for earnings. You’ll see how the policy links to hiring, retention, training, and workforce mobility.

In this article, you’ll get clear, practical views of likely employment effects, tax questions, and what pilots can reveal about behavior and well‑being. That context helps you plan for changes that might affect your organization and your people.

Key Takeaways

- You’ll learn why the policy is seen as a stabilizing floor during shocks.

- Urban pilots and private grants have informed practical lessons.

- Research suggests benefits to well‑being with mixed effects on work.

- Design choices shape tax implications and public reaction.

- You’ll get pointers to adapt hiring, scheduling, and development plans.

What You Mean by Universal Basic Income and How It Works

Think of it as a predictable cash floor: regular transfers that arrive whether you work or not. Fabian Wendt describes this model as a scheduled payment—monthly or yearly—given without tests for work, wealth, or family status.

Core features are simple and reduce paperwork. Every eligible adult gets regular cash with no behavioral conditions. You won’t need to prove job searches or report small income changes to keep receiving payments.

How it differs from related designs

- Minimum Income Guarantee: tops up earnings to a set threshold rather than giving everyone the same transfer.

- Negative Income Tax: adjusts benefits through the tax system as your earnings change, as Milton Friedman proposed.

- Delivery way matters: direct payments give predictability; tax-based routes alter timing and how benefits integrate with existing systems.

MacKay and others note common U.S. proposals use amounts like $1,000/month as an example. Studies and city pilots help you anticipate behavioral responses, while financing options—income, sales, or capital tax—shape who gains or pays.

For practical details, see a short overview of delivery and transactions in this payment delivery way.

Why UBI Is Back on the Agenda in the United States

Pandemic-era relief and rising automation fears rekindled interest in regular cash as a policy tool.

During the pandemic, one-time stimulus checks showed how quickly Washington can move — and how limited a single payment can be when people face ongoing shocks.

Mayors for a Guaranteed Income helped push pilots in several cities. Jack Dorsey’s $15 million gave private backing to tests like the Durham idea that planned $500/month for 55 formerly incarcerated people until recovery.

Pandemic shocks and income volatility

You saw momentum return because many people lost pay or work unexpectedly. Pilots tested recurring money over a set time to track spending, health, and job search behavior.

Automation anxiety and a high-profile example

Andrew Yang’s “Freedom Dividend” — a $1,000/month example — put fears about automation and fragile jobs on the national stage.

- Local pilots let states and cities learn what works before scaling.

- Lessons focus on how people budget recurring transfers versus one-time aid.

- Policymakers weigh benefits against taxes, fiscal costs, and admin trade-offs.

universal basic income: The Main Goals and Who Benefits

Policymakers and advocates frame the plan as a tool that reduces hardship and restores choice for people facing unstable work.

Anti-poverty aims and dignity

You’re weighing a policy designed to lower poverty by supplying steady cash to all eligible adults. MacKay and Wendt note that regular transfers cut the harm caused by delays, sanctions, and complex eligibility checks.

People keep control over spending, which reduces stigma and the need to prove hardship. That dignity matters for daily decisions and long-term planning.

Freedom, anti‑paternalism, and simplification

Supporters argue the idea shrinks bureaucracy and respects individual choice. Individuals can reallocate time to caregiving, retraining, or launching small ventures without losing support.

“Cash can change household bargaining power, especially for women who gain independent resources for childcare or safety choices.”

You’ll weigh trade-offs: keep targeted benefits or replace them, and decide which design meets your goals for equity and efficiency. For how this links to labor shifts and automation, see this analysis on automation and jobs.

- Stable transfers reduce errors and administrative friction for agencies and people.

- Universal coverage lowers stigma and reframes support as shared rather than targeted at others.

- Design choices determine who benefits most and where need is most urgent in your community.

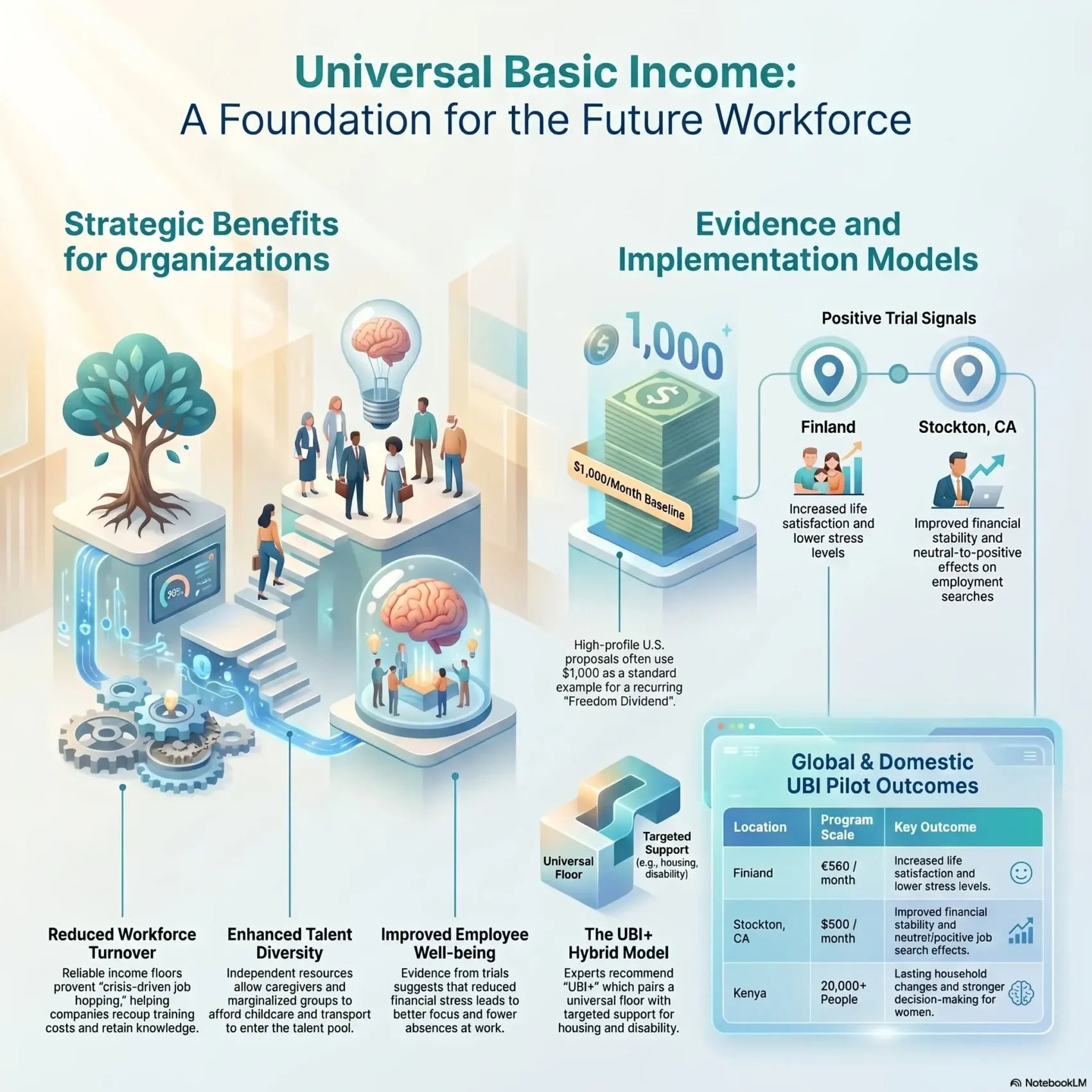

Pros for Your Future Workforce and Organization

Predictable cash can reshape how your workforce plans careers and copes with short-term shocks.

Income stability that supports employment, training, and better job matches

Steadier income reduces crisis-driven job hopping. When people have a reliable floor, they can invest time in training and wait for roles that fit their skills.

Evidence from Finland’s trial and Stockton’s pilot shows improved life satisfaction and hints at positive work signals. That may translate into clearer growth paths and longer tenure.

Mental health and well-being gains

Wendt and MacKay highlight dignity and fewer sanctions as drivers of better mental health. Less stress means fewer absences and better focus on tasks.

Diversity and inclusion: support for caregivers and marginalized groups

You may expand your talent pool as caregivers, women, and other groups gain resources to arrange childcare for children or pay for transport and courses.

- More reliable scheduling from steadier cash flows.

- Higher employment quality as people avoid desperation hires.

- Teams that feel respected show lower turnover and stronger inclusion.

Track pilot evidence to adapt benefits, training, and wellness supports so your organization can make the most of this changing environment.

Cons You Need to Weigh Before Backing a UBI Policy

You’ll want to look beyond the promise of steady checks and examine who pays, who benefits, and how work incentives shift.

Cost, taxes, and public resistance

Generous plans carry high fiscal cost. International analyses show large budgets are required for big payments and that can prompt higher tax rates.

You must compare headline cost with who pays and who gains. Even if many people net out ahead, broad taxes can reduce support.

Designs that use income tax or other levies try to ensure higher earners become net contributors. Still, voters often resist perceived payments to the wealthy.

Labor supply concerns and reciprocity debates

Some worry that ubi would lead some workers to cut hours or delay job entry. Yet studies show mixed effects that depend on payment size and tax changes.

Reciprocity matters in U.S. politics: many expect public support to be linked to work or training. Removing conditions can fuel backlash.

- Evaluate headline cost and distribution: who gains, who pays.

- Anticipate political sensitivity about unconditional cash and rich recipients.

- Model labor-supply and economy-wide effects before committing to major reform.

What the Evidence and Trials Tell You

Trials around the world give clear signals about how steady cash affects people’s work, health, and choices.

Finland’s randomized trial

Finland gave €560 per month to unemployed people and tracked outcomes for two years. Recipients reported higher life satisfaction and lower stress, and researchers saw small positive employment signals.

Stockton and U.S. pilots

The SEED pilot in Stockton provided $500/month as regular cash. Results showed better financial stability and neutral to positive effects on jobs and work search for many people.

Kenya and Manitoba lessons

GiveDirectly’s long trials across roughly 20,000 people over years show lasting household changes and stronger decision-making by women.

Manitoba’s 1970s Mincome offered early community-level evidence on family dynamics and local labor patterns.

Limits of pilots

Pilots do well at measuring household behavior, but they rarely test the tax and funding systems a national roll-out would need.

- Small scale vs. economy‑wide tax effects

- Short timelines for long-term fiscal impact

- Context differences across countries and cities

Use these studies as practical evidence to stress-test your workforce assumptions before scaling policy responses.

How UBI Might Be Funded and What That Means for You

Funding choices will shape who keeps more of each paycheck and who becomes a net contributor. You’ll want to see how revenue plans change take-home pay, hiring costs, and benefits budgeting.

Income tax changes, removing personal allowances, and taper rates

Many proposals rely on adjusting the income tax base. Policymakers often consider removing tax-free personal allowances and raising marginal rates to pay for regular payments.

That move changes net pay across your workforce and alters payroll planning. Taper rates matter because they decide how quickly support phases out as income rises.

Balanced approaches: wealth, sales, and carbon taxes

To avoid very high income tax rates, proposals often mix revenue sources. Wealth levies, targeted sales taxes, or carbon charges can spread the cost and improve perceived fairness.

Winners and losers across households, children, and lone parents

Research shows distributional outcomes vary by design. Some plans reduce overall poverty but can harm children or lone parents unless targeted supports remain.

“UBI+ models often keep housing, disability, and child supports to avoid unintended harms.”

- Map state and federal flows to see net effects on paychecks.

- Use refundable credits and targeted benefits to protect vulnerable groups.

- Budget for admin and communication so employees understand changes.

Policy Design Choices That Change the Impact

The devil is in the details: small design moves decide whether a reform cuts poverty or creates gaps. You’ll weigh several trade-offs when reviewing proposals and running scenarios for your region.

Payment levels: below benefits, near poverty line, or Minimum Income Standard

Comparative analyses show higher payments—close to a Minimum Income Standard—can sharply reduce poverty but demand large tax changes and public spending. Lower payments are cheaper and still help some people, but they do less to lift households above the poverty line.

UBI+ models: why housing, disability, and child costs still need targeted support

UBI+ keeps targeted benefits for housing, disability, and child costs to avoid one-size-fits-all failures. Studies find distributional results vary: some proposals lower overall poverty while disadvantaging specific households unless calibrated.

- Include a child add-on or child‑specific payments so families aren’t penalized.

- Model tapering and benefit interactions to see how work incentives change for individuals at different earnings levels.

- Plan payroll and tax withholding changes so your employees experience predictable net income shifts.

Use scenario planning to test recruitment, retention, and internal mobility under different payment levels. Target safeguards so people in or near poverty do not face net losses during any transition.

UBI in Practice: U.S. Pilots, City Programs, and Child Tax Credit Learnings

City-level pilots gave policymakers a rare chance to test monthly cash grants under real-world conditions.

Mayors for a Guaranteed Income launched pilots across several cities, backed in part by Jack Dorsey’s $15 million gift. Local programs delivered monthly payments to defined groups to study take-up, trust, and short-term effects on work and housing.

Targeting formerly incarcerated people

Durham’s proposal to provide $500/month to 55 formerly incarcerated people tested reentry supports. These people often face job and housing barriers and restrictions on programs like SNAP.

Expanded Child Tax Credit as a child-focused model

The expanded Child Tax Credit served as an example of monthly child payments. Parents received predictable money and could decide how to spend it on essentials for children.

- City pilots showed how eligibility, disbursement, and outreach shape trust and take-up over time.

- Targeting groups—like people reentering communities—gave insights on housing stability and job search outcomes.

- Child-focused monthly payments acted like a baseline for families, improving predictability for bills and childcare.

“Pilots offer useful signals, but trials rarely model tax or macro effects, so you must combine local data with broader fiscal scenarios.”

What UBI Could Mean for Employers and Workforce Planning

Expect practical changes in hiring, retention, and how people balance work and life when steady cash support becomes common.

Turnover, wages, and job quality pressures

Evidence from Finland and Stockton shows better well‑being and some positive work signals after pilots of a universal basic income.

You may see reduced turnover because workers face fewer emergency exits. That helps you recoup training costs and boost institutional knowledge.

At the same time, some roles may feel pressure. Workers can hold out for safer schedules and clearer career paths, which can push wages and improve job quality.

Gig work, part-time roles, and entrepreneurship pathways

When a steady payment covers essentials, recruiting for part-time or gig positions may get easier. Flexibility becomes more attractive to people seeking autonomy.

Some employees will use resources to start side businesses or pursue education. That creates new internal mobility and retention choices for your teams.

- Lower turnover lets you invest more in training and career ladders.

- Expect mixed hour patterns: some reduce hours for caregiving or school; others pursue higher-responsibility jobs.

- Use example scenarios to stress-test staffing and tax-driven cost changes at the economy level.

Plan proactively: pair benefits and wellness programs with clear career pathways so your organization captures the positive impact while managing transition risks.

Conclusion

Conclusion

Evidence from Finland, Stockton, Kenya, and Manitoba gives you clear signals: better life satisfaction and modest positive employment outcomes in trials, plus longer‑term community effects in larger studies.

Policy choices matter. Well‑designed proposals that pair a universal basic income with targeted supports can cut poverty while limiting winners and losers. Funding, taxes, and cost trade‑offs will shape feasibility and public support.

For your organization, apply the research to workforce planning. Track pilots, push for transparent data, and weigh incremental steps like child credit expansions. That way you help shape a policy that improves life for people while keeping fiscal and administrative realities in view.